Issuer repurchases of equity securities

In brief

On May 3, 2023, the Securities and Exchange Commission (SEC) adopted new rules to modernize and enhance the disclosure requirements for repurchases of equity securities by publicly listed companies, often referred to as stock buybacks. Among other changes, the amendments will require issuers to disclose in their periodic reports their daily share repurchase activity for each quarter (replacing the proposed rule that issuers would have to make daily filings of share repurchase activity) and provide certain additional narrative disclosure about their share repurchase programs in periodic reports. The SEC also adopted new Item 408(d), which will require disclosure in issuers’ periodic reports regarding the adoption and/or termination of 10b5-1 trading arrangements during the reporting period.

Key takeaways

The newly adopted amendments are intended to improve existing disclosure obligations related to issuer repurchases by requiring disclosure of the following (which must be tagged in Inline XBRL):

- Quantitative daily repurchase activity for the most recently completed quarter as an exhibit to Form 10-K and Form 10-Q (Form N-CSR for listed closed-end funds and new Form F-SR for foreign private issuers) and eliminating the requirement in current Item 703(a) to disclose repurchase data on a monthly basis.

- The structure of an issuer’s repurchase program(s) and its share repurchase activity, including the objectives or rationales for each repurchase, any policies or procedures relating to purchases by an issuer’s directors and officers subject to the reporting requirements under Section 16(a) of the Exchange Act (“Section 16 Officers”) during a repurchase program and the timing of certain transactions by directors and Section 16 Officers leading up to or following the announcement of a repurchase plan.

- The issuer’s adoption or termination of a contract, instruction or written plan to purchase or sell its securities during the most recently completed fiscal quarter that was intended to satisfy the affirmative defense conditions of Rule 10b5-1(c), as well as a description of the material terms of such arrangement.

In the adopting release, the SEC indicated that the amendments will help investors better understand issuers’ motivations for conducting share repurchases and the extent of an issuer’s activity in the market. The amendments are also intended to provide insights into any potential relationships between share repurchases and executive compensation and stock sales to protect investors from information asymmetries between issuers, directors, executives and investors. There are no exemptions from these disclosure requirements under the final rules.

In depth

After the initial proposing release in December 2021, the SEC received over 170 unique comment letters during three comment periods. The final rules include certain modifications to the rules as initially proposed, including:

- As proposed, the amendments would have required daily repurchase disclosures on a new Form SR, which would be furnished to the SEC one (1) business day following an issuer’s share repurchase. The final amendments modify the frequency and manner of this disclosure requirement and require that daily repurchase activity be disclosed in issuers’ periodic reports. The disclosures under the final rules must also be filed with the SEC instead of furnished.

- The proposed amendments would have required disclosure via checkbox above the tabular repurchase disclosures indicating whether the issuer’s directors or Section 16 Officers made transactions in the class of equity securities subject to an issuer repurchase plan within ten (10) days before or after the issuer’s announcement of a repurchase plan. The final rules reduced the window triggering disclosure to four (4) business days.

- The final rules modify the manner in which issuers must report information relating to Rules 10b5-1 and 10b-18. The originally proposed Form SR would have required issuers to make tabular disclosures of the number of shares purchased in reliance on Rule 10b-18 or intended to qualify for the affirmative defense provisions of Rule 10b5-1(c). In light of the elimination of Form SR in the final rules, issuers will be required to provide these tabular disclosures in their periodic reports, including footnote disclosure regarding the date a plan was adopted or terminated.

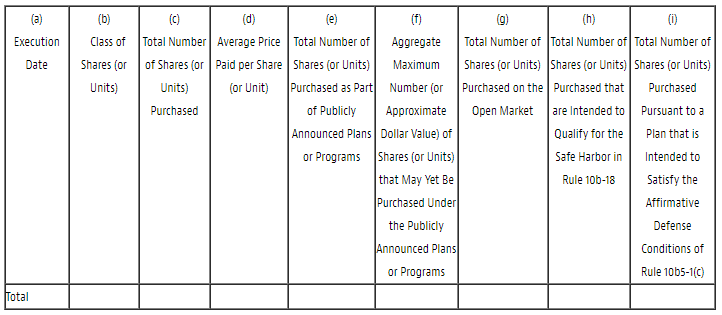

Specifically, the newly adopted provisions of Item 703 require the following tabular and narrative disclosures:

Tabular Disclosure: Quantitative daily repurchase information in each periodic report in the following format, including checkbox disclosure immediately preceding the tabular disclosure if any director or Section 16 officer traded in the issuer’s securities within four (4) business days before or after the announcement of any share repurchase plan or program during the quarter:

Issuer Purchases Of Equity Securities

Use the checkbox to indicate if any officer or director reporting pursuant to Section 16(a) of the Exchange Act (15 U.S.C. 78p(a)), or for foreign private issuers as defined by Rule 3b-4(c) (§ 240.3b-4(c) of this chapter), any director or member of senior management who would be identified pursuant to Item 1 of Form 20-F (§ 249.220f of this chapter), purchased or sold shares or other units of the class of the issuer’s equity securities that are registered pursuant to Section 12 of the U.S. Securities Exchange Act of 1934, as amended, and subject of a publicly announced plan or program within four (4) business days before or after the issuer’s announcement of such repurchase plan or program or the announcement of an increase of an existing share repurchase plan or program.

Narrative Disclosure: Referencing the tabular disclosures discussed above as appropriate, issuers will also be required to disclose:

- The objectives or rationales for each repurchase plan or program and process or criteria used to determine the amount of repurchases.

- Any policies and procedures relating to purchases and sales of the issuer’s securities by its officers and directors during a repurchase program, including any restriction on such transactions.

- The existing disclosures required by Item 703 with respect to repurchases made through a publicly announced plan or program or otherwise during the reporting period.1

Finally, new Item 408(d) provides for new disclosure requirements concerning issuers’ Rule 10b5-1 plans and similar trading arrangements, which are intended to complement the amendments to Item 7032. Item 408(d) requires issuers to disclose:

- Whether the issuer adopted or terminated any contract, instruction or written plan to purchase or sell its securities during the most recently completed fiscal quarter that was intended to satisfy the affirmative defense conditions of Rule 10b5-1(c).

- The material terms of such contract or arrangement, including: the date of adoption or termination, the duration of the arrangement and the aggregate number of securities to be purchased or sold thereunder.

Foreign Private Issuers: Foreign private issuers who do not file on domestic forms will be required to file a quarterly report of their daily share repurchase activity on Form F-SR, which would be substantially similar to the disclosure requirement for domestic issuers. The Form F-SR will be due within 45 days of the end of the fiscal quarter.

Further, foreign private issuers will be required to check a box if any of their directors or senior management who would be identified in Item 1 of their Form 20-F traded in the issuer’s securities within four business days before or after the announcement of any share repurchase plan or program.

Implementation Timeline: Domestic issuers will be required to comply with these amendments beginning with the periodic report covering the first full fiscal quarter beginning on or after October 1, 2023. Foreign private issuers will be required to comply with these amendments beginning with the Form F-SR that covers the first full fiscal quarter that begins on or after April 1, 2024. The Form 20-F narrative disclosure will be required in the first Form 20-F filed after the first Form F-SR.

More Information

- Fact Sheet: Share Repurchase Disclosure Modernization

- Final rule: Share Repurchase Disclosure Modernization

1 Issuers should keep in mind when preparing these disclosures that all repurchase activity is covered are covered by the rules, including e.g. surrendering vested shares back to the issuer to satisfy withholding taxes on share awards. On the other hand, net settlement of RSUs on vesting or “sell-to-cover” arrangements where the plan administrator sells shares on the open market, would not be treated as issuer share repurchases for purposes of the disclosure. See the SEC’s CDI 149.01.

2 Item 408(d)(1) will include a footnote providing that if the issuer has made disclosure pursuant to Item 703 that would satisfy the requirements of Item 408(d)(1), the issuer may cross-reference to such disclosure to avoid duplicative disclosure.