In brief

On 19 September 2023, the EU Commission opened a consultation on its BEFIT Directive, which was published the previous week. BEFIT is the acronym for Business in Europe: Framework for Income Taxation. The initiative, widely considered to replace the EU Commission’s Consolidated Common Corporate Tax Base (“CCCTB”), will aim to introduce a common set of rules for groups of companies and head offices, based in the EU, to determine their taxable base. The BEFIT proposal could also apply to non-EU-headquartered groups. It will allocate the companies’ profits between the relevant EU member states and, according to the Commission, it will reduce compliance costs for in-scope businesses by up to 65%.

Stakeholders have been asked to provide feedback on the new proposal by 15 November 2023.

Contents

Background

The Commission announced BEFIT on 18 May 2021, as part of its communication on Business Taxation for the 21st Century. BEFIT was proposed as a single corporate tax rulebook for the EU, based on a formulary apportionment and a common tax base.

Currently, businesses operating cross-border within the internal market are potentially subject to, and must deal with, 27 different corporate tax systems of the respective member states. In an attempt to simplify the tax environment in which these businesses operate, the Commission has proposed this common framework for corporate tax rules, which should largely replace the current domestic corporate tax systems for in-scope taxpayers. However, the proposal does not provide for a full harmonisation of the corporate tax systems. For example, member states will maintain the ability to set their own national corporate tax rates and will be able to apply upward and downward adjustments to the BEFIT taxable base. Individual member states will also remain responsible for enforcement and audit policies, but will work in close cooperation with other member states where in-scope taxpayers are resident.

Application

The purpose of the proposal is to lay out a common set of rules as a basis to determine the taxable income of (large) groups of companies and companies with permanent establishments in the EU. It therefore lays down rules to calculate the tax base for these in-scope taxpayers. Specifically, BEFIT introduces a formula to calculate and allocate across member states the taxable income of a “BEFIT group”, i.e., the group of EU-resident companies and permanent establishments that are at least 75% owned by a common parent entity (note that this is a different group definition than under Pillar 2).

The application of BEFIT becomes mandatory for multinational groups headquartered in the EU with a consolidated annual revenue of at least EUR 750 million p.a. in at least two of the preceding four fiscal years. This threshold is similar to the CbCR and the Pillar 2 threshold. If the group’s ultimate parent entity is headquartered outside the EU, and the revenue threshold is met, BEFIT will apply if the group’s combined annual revenue in the EU is either EUR 50 million in at least two of the last four fiscal years or more or 5% or more of the total combined revenues of the group originates in the EU in at least two of the last four fiscal years. Taxpayers that do not meet the revenue thresholds may still elect to apply the BEFIT regime. The election applies for five years and can be extended. If the BEFIT thresholds are met or the BEFIT election is made, all entities and permanent establishments located in the EU that belong to the BEFIT group are in scope.

Mechanism of BEFIT

The BEFIT regime introduces a formula to calculate the taxable income of the BEFIT group and allocate it across the member states. The starting point for the aggregated tax base calculation is the commercial financial statements (before consolidation adjustments eliminating intra-BEFIT group transactions) of each BEFIT group member. The acceptable accounting standards for the commercial financial statements are the International Financial Reporting Standards (IFRS) or the local (national) Generally Accepted Accounting Principles (GAAP) of the ultimate parent entity’s member state if it is resident in the EU — or of the filing BEFIT entity if the ultimate parent entity is headquartered outside the EU.

The individual tax base shall be computed by making different adjustments, which include rules on interest limitation, an exclusion of capital gains and dividends, adjustments for foreign exchange results, amortization and depreciation, and adjustments for the inclusion of any qualified domestic top-up tax (QDTT) — the equivalent of the Qualified Domestic Minimum Top-Up Tax (QDMTT) under the Pillar 2 Directive. Bad debts may only be deducted under certain conditions and only if they did not result from a transaction with another BEFIT group member. In addition, the proposed Directive contains rules regarding attributing revenue, expenses and deductions derived from the operation of aircrafts and ships in international traffic, the operation of boats engaged in inland waterways transport and extractive activities. Specific rules are also included for business reorganizations and the recognition of intra-BEFIT group transactions prior to a BEFIT group member leaving or entering the group.

As a next step, the calculated preliminary tax results of the BEFIT group members are aggregated to calculate the tax base at the level of the BEFIT group. If a BEFIT entity’s tax base is positive, it is aggregated to determine the BEFIT tax base of the BEFIT group. If a BEFIT entity’s tax base is negative, it will be included in the BEFIT tax base, but its baseline allocation percentage (used in the next step to allocate the BEFIT tax base to the different taxpayers within the BEFIT group) will be set to 0% during the transitional phase (see below). Cross-border loss relief will thus be made possible (like it was foreseen under the CCCTB proposal) and will be automatically applied. This is currently only possible on rare occasions and under stringent conditions. If the aggregated BEFIT tax base is a negative amount (i.e., a loss), the loss will be carried forward indefinitely in time to set it off against the future positive BEFIT tax bases.

Importantly, according to the proposal, only 95% of gains or losses deriving from dividends and capital gains on shares (provided a 10% ownership threshold and a one-year holding period are met) are excluded from the BEFIT tax base. Some member states, such as the Netherlands, Austria and Belgium, exclude 100% of such income under their current participation exemption regime, while countries such as Germany only exclude 95% in effect. While member states may continue to apply additional exemptions, in accordance with the proposed Directive, it appears that if member states introduce these additional exemptions, it may lead to a disparity and a lack of harmonization, which will undermine the goals of the BEFIT proposal.

Furthermore, the proposal stipulates that a company or a permanent establishment that is subject to this Directive shall cease to be subject to the national corporate tax law in all member states where it is established in respect of all matters regulated by this Directive, unless otherwise stated in the Directive. It would thus appear that entities in scope of, for example, the Dutch, Austrian or Belgian participation exemption regime may face a higher tax base calculation under the Directive, once they become BEFIT taxpayers. In addition, the proposed Directive does not address dividends and/or capital gains resulting from subsidiaries that are subject to the switchover rules under the Anti-Tax Avoidance Directive I (EU 2016/1164) or other domestic rules and which are taxable in the member state in which the parent is resident. These capital gains and dividends seem to be covered by the exclusion from the BEFIT tax base.

At the same time, member states would no longer be able to impose withholding taxes or any other source taxation on intra-BEFIT group transactions, unless the ultimate beneficial owner of the payment is not a BEFIT group member.

Transfer Pricing

The proposed Directive also simplifies transfer pricing compliance for limited risk distribution and contract manufacturing activities between BEFIT group members and non-BEFIT group affiliates (a so-called “traffic light system”).

Under the proposal, member states shall structure their risk assessment into three transfer pricing risk zones: low, medium and high. The activities of in-scope limited risk distributors or contract manufacturers would be risk assessed and slotted into one of the risk zones by way of comparing their profit performance to the five-year average interquartile range of the most recent set of EU-wide public benchmarks prepared before the end of the respective year and published by the EU Commission. An activity is considered low risk if the profit performance is above the 60th percentile of the public benchmark; it is considered medium risk if it is below the 60th but above the 40th percentile; and it is high risk if it is below the 40th percentile of the EU-wide public benchmark.

The transfer pricing results of low-risk activities shall not be further reviewed. Member states may allocate resources to monitor medium-risk activities, and they may suggest a revision of the transfer pricing policies or decide to initiate a review or audit in the case of high-risk activities. The profitability of limited risk distributors shall be measured based on an EBIT to sales profit level indicator, and the profitability of contract manufacturers shall be measured based on an EBIT to total costs profit level indicator. Member states are required to implement this simplified approach to transfer pricing compliance.

Compliance

The BEFIT group will file one BEFIT information return with the filing authority (i.e., the competent authority of the member state in which the filing entity is resident). The filing entity will be the ultimate parent entity if the group is headquartered in the EU. If a group is headquartered in a non-EU jurisdiction, the BEFIT group may appoint the filing entity for the BEFIT group members. Once a filing entity is appointed, in principle, it cannot be changed.

The BEFIT information return must be submitted within four months of the end of the fiscal year, which is a considerably shorter filing deadline than under most domestic laws. Given the fact that — similar to Pillar 2 — BEFIT requires adjustment calculations to the respective financial statements, a question arises regarding whether such filing deadline is feasible, given the substantial compliance burden. Amended returns can be filed within two months after a timely submission of the initial return. Upon filing the return, a “BEFIT team”, consisting of representatives of each EU member state’s tax administration in which the BEFIT group has group members, will examine the completeness and accuracy of the details provided in the BEFIT information return.

Individual members of the BEFIT group must still file an individual tax return with the competent authority of the member state in which it is resident, within three months of receiving the BEFIT information return notification, but no later than eight months after the end of the fiscal year. An individual assessment will still be issued and may be (administratively) appealed within two months. Tax enforcement remains with the member state in which the individual entity is resident.

It is important to note that all BEFIT group members must have the same fiscal years, which must contain 12 months. It would, thus, no longer be possible to have different fiscal years for group companies that are also members of the BEFIT group.

Under the proposed Directive, concerned member states may initiate and coordinate audits of BEFIT group members. Audits and joint audits will be carried out in accordance with applicable domestic rules and in accordance with what is provided for in EU Directive 2011/16 for cross-border and joint audits.

Application of the BEFIT proposal

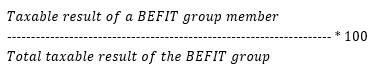

If the proposal is adopted in its current form, the provisions of the Directive will apply from 1 July 2028. A transitional period will apply from 1 July 2028 to 30 June 2035, during which the (positive) BEFIT tax base is allocated in accordance with a baseline allocation percentage:

The “taxable result of a BEFIT group member” is equal to the average of the taxable results in the three previous fiscal years of that particular BEFIT group member, and the “total taxable result of the BEFIT group” is equal to the sum of the average of the taxable results of all BEFIT group members in the three previous fiscal years. For allocation purposes, a negative preliminary tax result would be considered as zero. Intra-BEFIT group transactions shall be presumed to be at arm’s length if the expense incurred, or the income earned, by a BEFIT group member from intra-BEFIT group transactions increases in a fiscal year by less than 10% compared to the average expense or income of the previous three fiscal years from intra-BEFIT group transactions. If this 10% threshold is met or exceeded, the excess amount will be presumed not to be at arm’s length and will be disregarded for the purposes of computing the baseline allocation percentage of that BEFIT group member (with the possibility for the taxpayer to rebut the presumption).

By the end of the third year of the transition period, the Commission shall prepare a study on the possible composition and weight of selected formula factors, and it may adopt a legislative proposal during the transition period to amend the Directive by introducing a method for allocating the BEFIT tax base using formulary apportionment. In the absence of such further legislative changes, the allocation rules above will remain applicable.

The Directive, as a tax measure, requires unanimous consent from all 27 member states. Such consent is not easily obtained, and it is highly likely that the proposed Directive will be amended several times before a final act is adopted. If adopted in time, the Directive will be in force from 1 January 2028, and member states will need to implement the necessary legislation by then. The provisions will then apply to in-scope taxpayers from 1 July 2028.

Next steps

The Commission has opened the consultation process on the draft proposal and invited stakeholders to provide input and feedback by 15 November 2023. This is a great opportunity for multinational enterprises to address the technical provisions of the proposal as well as administrative and compliance burdens.

Baker McKenzie has extensive experience in drafting feedback submissions and advising clients on tax policy matters. Should you wish to provide feedback to this consultation, please reach out to your local Baker McKenzie contact.