Recent developments

On 16 November 2018, the Stock Exchange of Hong Kong Limited (SEHK) published: (1) the findings of its latest review of listed companies’ corporate governance; and (2) updated guidance materials on environmental, social and governance (“ESG“) reporting. The implications of these materials are twofold.

Firstly, SEHK reminds listed companies that the amendments to the Corporate Governance Code and related Listing Rules (“CG Code amendments“) will take effect on 1 January 2019. For a summary of the CG Code amendments, please see our client alert titled “Corporate Governance Code will tighten INED’s independence assessment criteria in

2019″.

Secondly, the updated ESG guidance materials address the increasing demand for ESG information disclosure. SEHK encourages listed companies to develop an ESG strategy to cope with such international trends and provide practical tools to enhance the preparation of ESG reports. Listed companies can follow those steps and procedures voluntarily, or develop their own procedures in view of their specific circumstances.

Implications

The following table has summarized the major implications of the relevant

documents:

| Document title | Implications |

| 1. Analysis of Corporate Governance Practice Disclosure in June and December Year-End 2017 and March Year-End 2018 Annual Reports (“CG Report Review“) | Regarding non-compliant mandatory disclosure requirements and recommended disclosures, SEHK reminds listed companies not to resort to sweeping statements or use “boiler-plate” language. Instead, listed companies should: (1) Set out the circumstances that are unique to the company to explain such departure; (2) Make clear and complete disclosures or provide reasons for any non-disclosures; and (3) Use cross-referencing links to minimize repeated disclosures. |

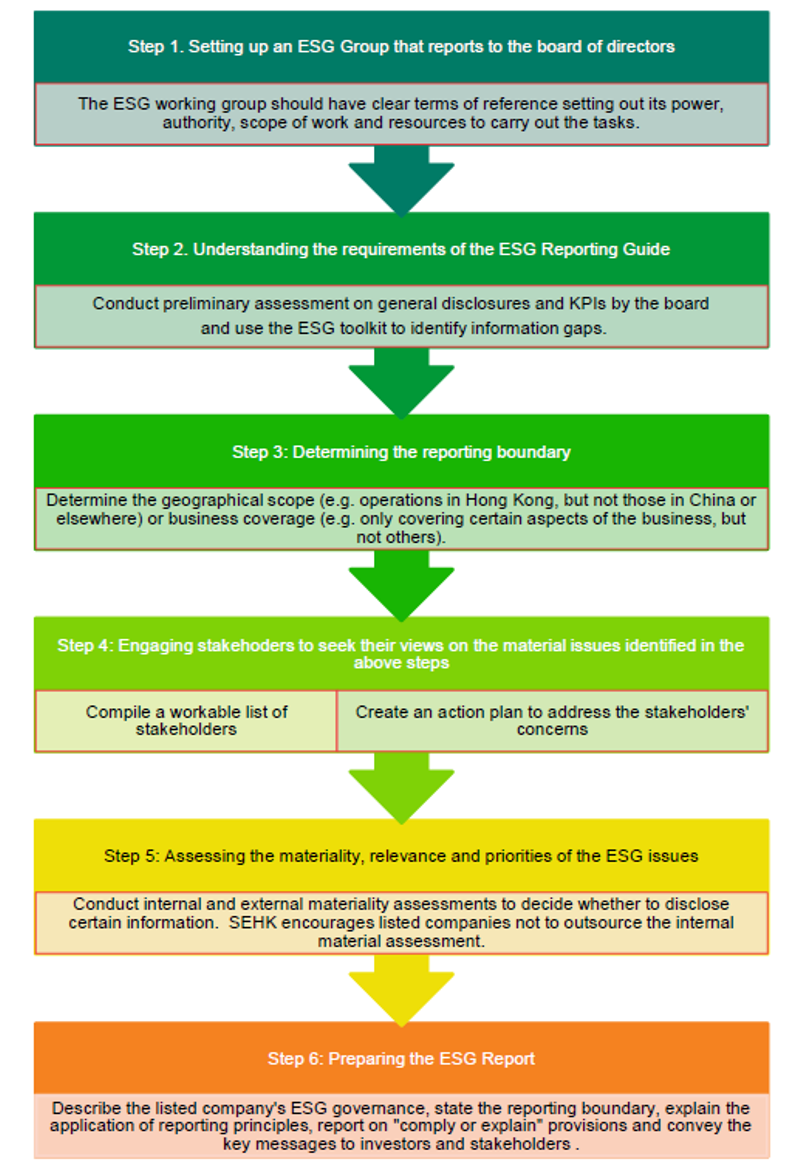

| 2. How to prepare an ESG report? A step-by-step guide to ESG reporting (“ESG guideline“) | SEHK proposes the following steps to prepare an ESG report: (1) Establish an ESG working group; (2) Understand the ESG requirements and identify information gaps; (3) Determine the geographical or business boundaries for reporting purpose; (4) Assess stakeholder’s engagement; (5) Conduct internal and external materiality assessments; and (6) Prepare the ESG report that includes the findings in the above steps. |

| 3. How to prepare an ESG report? Appendix 1: Toolkit (“ESG toolkit“) | Use the ESG toolkit to determine: (1) Stakeholder’s dependence and influence on the listed company; (2) Stakeholder group’s identity and profile; (3) Stakeholder engagement plan, action plan and contingency plan; (4) Post stakeholder engagement action plan and timeline; and (5) Materiality and relevance of the information for general disclosures and key performance indicators (“KPI“). |

| 4. How to prepare an ESG report? Appendix 2: Reporting Guidance on Environmental KPIs (“ESG KPI guideline“) |

What to report? How to report? Use the methodologies and guidance to collect information and calculate the data called for under each of the KPIs in the environmental section of the ESG Report. |

| 5. Frequently Asked Questions on ESG reporting (“ESG FAQ“) | A listed company with operations in the PRC should consider the potential impact of the Environmental Protection Tax Law, which came into effect in China on 1 January 2018. |

Why does SEHK update the guidance materials on disclosure of environmental information?

On 21 September 2018, the Securities and Futures Commission (SFC) released its Strategic Framework for Green Finance (“SFC Framework“), which was based on the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) of Financial Stability Board. As part of the TCFD regulatory development, China is working to impose mandatory requirements for listed companies to disclose environmental information by 2020 and extend the mandatory requirements to A/H shares companies listed

on SEHK.

To align with TCFD recommendations and work along with China’s policy direction to target mandatory environmental disclosure, the SFC Framework outlines (1) its top priority to enhance Hong Kong listed companies’ disclosure of environmental information and (2) cooperation with SEHK to promote these initiatives. SEHK’s guidance materials on ESG reporting are the latest products of the TCFD recommendations.

What are the objectives of disclosing environmental information?

The TCFD recommendations focus on helping listed companies to identify, assess and disclose the impact of climate change-related risks and opportunities on their financial statements under the following four thematic areas:

- Corporate governance

- Business strategies under different climate-related scenarios

- Risk management

- Metrics and targets to manage the identified risks and disclose material information.

What are the steps and procedures to prepare an ESG report?

The ESG guideline recommends the following procedures:

Next steps

In anticipation of (1) the CG Code amendments effective on 1 January 2019 and (2) the upcoming consultation regarding the amendments of ESG-related Listing Rules in mid-2019, listed companies may consider to take the following actions:

- Assign senior management and staff to establish an ESG working group to determine whether to follow SEHK’s recommended steps or to develop its tailor-made procedures in view of the listed company’s specific circumstances.

- Review the ESG guideline, ESG toolkit, ESG KPI guideline and ESG FAQ for further details on the who, what, where and how.

- Visit the ESG section of SEHK’s website for additional international guidelines and calculation methods for KPIs.

- Review SEHK’s one-hour E-Training webcast entitled “INEDs’ Role in Corporate Governance” (“E-training“) after its publication expected before the end of 2018. The E-training will provide demonstrations with case scenarios and multiple choice questions and answers on CG Code amendments, INEDs’ role in corporate governance and additional measures for issuers with weighted voting rights.

[maxbutton id=”8″]