Background to DAC6

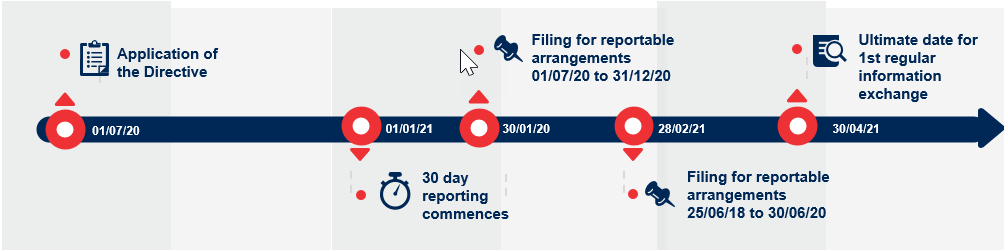

The EU mandatory disclosure regime known as DAC6 goes live on 1 July 2020 and reporting obligations were set to begin within 30 days from that date.

Under the wide-ranging DAC6 regime, intermediaries (such as tax advisors but in some cases extending to non-tax personnel) will have to report cross-border transactions going back to 25 June 2018 to EU tax authorities. The reporting obligation reverts to the taxpayer where there is no intermediary involved or legal professional privilege prevents the intermediary from reporting.

Arrangements are in scope if they involve either two EU member states or one EU member state and a third state and the transaction contains certain “hallmarks” that suggest potentially aggressive tax planning. Some of these hallmarks apply even where obtaining a tax advantage is not the main benefit, or one of the main benefits, of the transaction. This means that many commercially-driven transactions could fall within the regime and need to be reported. Failure to report could result in significant penalties, which vary considerably among member states and which, in limited cases, include criminal liability.

Option for six month delay to reporting

The proposal for a deferral of time limits was a response to the severe disruption caused by the COVID-19 pandemic. The three-month deferral was not deemed adequate by some EU member states and agreement has now been reached on a six-month deferral. However the draft Directive makes it clear that the deferral will be optional for member states.

The DAC6 mandatory disclosure regime will still apply from 1 July 2020 and, if member states exercise this option, the following amendments will apply:

- the deadline for filing information in respect of reportable cross-border arrangements implemented in the period between 25 June 2018 to 30 June 2020 (originally 31 August 2020) will be postponed to 28 February 2021 (a six-month delay);

- The deadline for the first automatic exchange of information on reportable cross-border arrangements between member states will also be deferred from 31 October 2020 to 30 April 2021;

- Where a reporting obligation arises between 1 July 2020 and 31 December 2020 the period of 30 days for reporting begins on 1 January 2021 and will thus end (for all reportable matters arising in that period of six months) on 30 January 2021 (which thus becomes the new filing deadline for that entire period of six months). The reporting obligation for that period might be triggered by (a) the implementation of the first step of a reportable cross-border arrangement, (b) the fact that an arrangement becomes ready for implementation, (c) the fact that an arrangement is made available for implementation or (d) the fact that an intermediary provides aid, assistance or advice in relation to a reportable arrangement, all within that period of six months; and

In the case of marketable arrangements, the first periodic report will have to be made by the intermediary by 30 April 2021 at the latest.

The draft Directive also allows for a further three-month extension of the time limits if “severe hindrances, economic disturbance and risks for public health caused by the COVID-19 pandemic continue to exist and Member States implement lockdown measures”.

So far, Belgium, Luxembourg and Sweden have made announcements that they expect to adopt the deferral in full should the draft Directive be agreed. The authorities in the UK have stated that they intend to wait until “the proposals are finalised” before confirming how this will apply to the UK’s rules.

The deferral must be unanimously approved by the Economic and Financial Affairs Council (ECOFIN). A European Parliament (EP) opinion is also required and is expected by 30 June 2020. Furthermore, the opinion of the European Economic and Social Committee is expected by 14 June 2020.

On the basis that the draft Directive, once approved, may be adopted at the discretion of each member state, it is imperative that businesses do not delay in preparing to meet their existing compliance obligations should reporting dates not be deferred (or not be deferred in all Member States where they operate).