In brief

On 2 May 2024, Decree No. 378/2024 (“Decree“) was published in the Official Gazette, extending the deadline for repatriating financial assets of at least 5% of the total value of the assets located abroad until and including 31 May 2024.

As a reminder, the applicable Personal Assets Tax (PAT) rates for assets located abroad will be the same as those applicable to assets located in Argentina if taxpayers repatriate financial assets of at least 5% of the total value of the assets located abroad before 31 March of each year and if certain additional requirements are met.

In depth

On 2 May 2024, the Decree was published in the Official Gazette, whereby the deadline for repatriating financial assets of at least 5% of the total value of the assets located abroad was extended until and including 31 May 2024.

As a reminder, the PAT rates applicable to assets located abroad will be the same as those applicable to assets located in Argentina if taxpayers repatriate financial assets of at least 5% of the total value of the assets located abroad before March 31 of each year. In that case, the tax rates corresponding to assets located in Argentina will be applicable if the following requirements are met:

- The repatriated funds remain deposited in an account (savings bank, current account, time deposit, etc.) opened in the name of its holder in Argentine financial institutions until 31 December of the year in which the repatriation was verified.

- The funds are sold in the free and single foreign exchange market, through the financial entity that received the funds from abroad.

- The acquisition of certificates of participation and/or debt securities of productive investment trusts set up by the Banco de Inversión y Comercio Exterior is recorded, provided that the investment remains under the ownership of the taxpayer until 31 December of the year in which the repatriation took place.

- The subscription or acquisition of shares of mutual funds that comply with the requirements of the National Securities Commission is recorded, provided that they remain under the ownership of the taxpayer until 31 December of the year in which the repatriation took place.

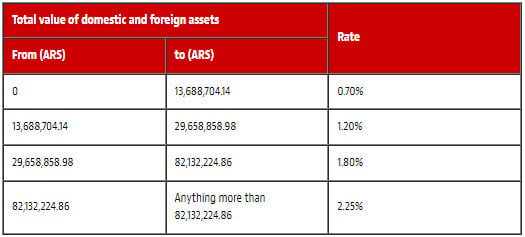

The tax rates applicable to assets located in Argentina are as follows:

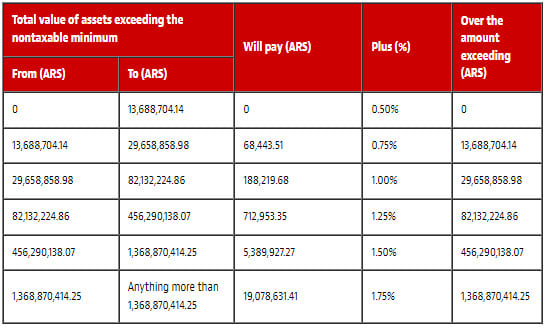

Likewise, the applicable tax rates on assets located abroad are as follows: